What Cost Is Not Included In The Real Prices Of Goods And Services?

In microeconomic theory, the opportunity toll of a detail activity option is the loss of value or benefit that would be incurred (the cost) by engaging in that activity, relative to engaging in an alternative activity offering a college return in value or benefit.

The smaller the opportunity cost, the greater the comparative advantage. For example, if you buy a automobile and use information technology exclusively for travel, y'all cannot rent it, whereas if yous rent information technology you cannot use it for travel. More simply, it ways you give up one affair for another.

In basic equation form, opportunity toll can exist divers as:

- Opportunity Price = (returns on best Forgone Option) - (returns on Chosen Selection)[1]

The opportunity cost of mowing 1's ain lawn for a md or a lawyer (who might otherwise make $100 an hour if they elected to work overtime during that fourth dimension instead) would be college than for a minimum-wage employee (who in the United States might earn $7.25 an 60 minutes), which would make the sometime more likely to hire someone else to mow their lawn for them.

Equally a representation of the relationship betwixt scarcity and choice,[2] the objective of opportunity cost is to ensure efficient use of deficient resources.[3] It incorporates all associated costs of a determination, both explicit and implicit.[4] Opportunity cost also includes the utility or economical do good an individual lost, if it is indeed more than than the monetary payment or actions taken. As an case, to go for a walk may not take whatsoever financial costs imbedded in to it. Yet, the opportunity forgone is the fourth dimension spent walking which could take been used instead for other purposes such every bit earning an income.[iii]

However, time spent chasing after an income might accept wellness problems like in presenteeism where instead of taking a ill 24-hour interval one avoids it for a salary or to exist seen as existence active.

A production possibility frontier shows the maximum combination of factors that can be produced. For case, if services were on the 10-axis of a graph and there were to exist an increment in services from 20 to 25, this would lead to an opportunity cost for the appurtenances that are on the y axis, as they would drop from 21 to 16. This means that every bit a result of the increase in consumption of services, the opportunity toll would exist those five goods that accept decreased.[5]

Regardless of the fourth dimension of occurrence of an activity, if scarcity was non-existent then all demands of a person are satiated. It's but through scarcity that choice becomes essential, since the use of scarce resources in ane way prevents its use in another way, resulting in the need to make a selection and/or decision.[2] These decisions are in turn exposed to multiple option outcomes.[half dozen]

Cede is a given measurement in opportunity cost of which the decision maker forgoes the opportunity of the adjacent best culling.[vii] In other words, to disregard the equivalent utility of the best culling choice to gain the utility of the best perceived option.[8] If there are decisions to be made that crave no sacrifice then these are price gratuitous decisions with zero opportunity cost.[nine] Through the analysis of opportunity price, a company can choose a path where the actual benefits are greater than the opportunity cost, and so that limited resources can be optimally allocated to achieve maximum efficiency.

When choosing an option among multiple alternatives, the opportunity cost is the gain from the alternative we forgo when making a conclusion.[10] In simple terms, opportunity toll is our perceived benefit of not choosing the next best option when resources are limited.[11] Opportunity costs are non limited to monetary or financial costs.[12] The actual toll of lost fourth dimension, lost product, or any other for-turn a profit benefit shall also exist considered an opportunity toll.[12] Opportunity cost is a key concept in economic science, described as the fundamental relationship between scarcity and choice.[eleven]

Types of opportunity costs [edit]

Explicit costs [edit]

Explicit costs are the straight costs of an action (business operating costs or expenses), executed either through a cash transaction or a concrete transfer of resource.[iv] In other words, explicit opportunity costs are the out-of-pocket costs of a firm, that are easily identifiable.[13] This means explicit costs will always have a dollar value and involve a transfer of money, eastward.g. paying employees.[14] With this said, these particular costs can hands be identified under the expenses of a business firm'south income statement and rest sheet to represent all the greenbacks outflows of a firm.[15] [14]

Examples are every bit follows:[13] [16]

- Country and infrastructure costs

- Operation and maintenance costs—wages, rent, overhead, materials

Scenarios are as follows:[xv]

- If a person leaves piece of work for an hour and spends $200 on function supplies, so the explicit costs for the private equates to the total expenses for the function supplies of $200.

- If a printer of a company malfunctions, then the explicit costs for the company equates to the total amount to be paid to the repair technician.

Implicit costs [edit]

Implicit costs (also referred to as implied, imputed or notional costs) are the opportunity costs of utilising resources endemic past the firm that could be used for other purposes. These costs are often hidden to the naked eye and aren't fabricated known.[16] Unlike explicit costs, implicit opportunity costs correspond to intangibles. Hence, they cannot exist clearly identified, defined or reported.[fifteen] This means that they are costs that have already occurred within a project, without exchanging cash.[17] This could include a small business possessor not taking whatsoever salary in the beginning of their tenure every bit a way for the business concern to be more profitable. Every bit implicit costs are the result of assets, they are also not recorded for the use of accounting purposes because they do not correspond any monetary losses or gains.[17] In terms of factors of production, implicit opportunity costs allow for depreciation of goods, materials and equipment that ensure the operations of a company.[18]

Examples of implicit costs regarding production are mainly resource contributed by a business concern owner which includes:[thirteen] [eighteen]

- Human labour

- Infrastructure

- Time

Scenarios are as follows:[15]

- If a person leaves piece of work for an hour to spend $200 on part supplies, and has an hourly rate of $25, then the implicit costs for the private equates to the $25 that he/she could take earned instead.

- If a printer of a visitor malfunctions, the implicit cost equates to the total production time that could accept been utilized if the automobile did non break down.

Excluded from opportunity cost [edit]

Sunk costs [edit]

Sunk costs (also referred to as historical costs) are costs that have been incurred already and cannot be recovered. Equally sunk costs have already been incurred, they remain unchanged and should non influence present or future actions or decisions regarding benefits and costs.[19] Decision makers who recognise the insignificance of sunk costs then understand that the "consequences of choices cannot influence choice itself".[2]

From the traceability source of costs, sunk costs tin be direct costs or indirect costs. If the sunk cost can be summarized equally a single component, information technology is a direct cost; if it is caused by several products or departments, information technology is an indirect cost.

Analyzing from the composition of costs, sunk costs tin be either stock-still costs or variable costs. When a visitor abandons a sure component or stops processing a sure product, the sunk toll usually includes stock-still costs such every bit rent for equipment and wages, just it also includes variable costs due to changes in fourth dimension or materials. Usually, fixed costs are more likely to constitute sunk costs.

More often than not speaking, the stronger the liquidity, versatility, and compatibility of the asset, the less its sunk toll will be.

A scenario is given below:[20]

A company used $5,000 for marketing and advertising on its music streaming service to increase exposure to the target market and potential consumers. In the terminate, the campaign proved unsuccessful. The sunk cost for the company equates to the $v,000 that was spent on the market place and advertising means. This expense is to be ignored past the company in its futurity decisions and highlights that no additional investment should be made.

Despite the fact that sunk costs should be ignored when making future decisions, people sometimes make the error of thinking sunk cost matters. This is sunk cost fallacy.

Example:Steven bought a game for $100, merely when he started to play it, he constitute information technology was dull rather than interesting. But Steven thinks he paid $100 for the game, then he has to play information technology through.

Sunk cost: $100 and the price of the time spent playing the game. Assay: Steven spent 100 yuan hoping to complete the whole game experience, and the game is an entertainment activeness, just there is no pleasure during the game, which is already low efficiency, but Steven also chose to waste fourth dimension. And so it'south calculation more cost.

Marginal cost

The concept of marginal cost in economics is the incremental price of each new product produced for the entire product line. For example, if yous build a plane, information technology costs a lot of money, only when you lot build the 100th aeroplane, the toll will be much lower. When building a new aircraft, the materials used may be more useful, and then make as many shipping as possible from as few materials as possible to increase the margin of profit. Marginal cost is abbreviated MC or MPC.

Marginal cost: The increase in toll acquired by an additional unit of production is chosen marginal cost. Past definition, marginal cost is equal to change in total price (TC) (△TC) divided by the corresponding change in output (△Q) : Change in total cost/change in output: MC(Q)=△TC(Q)/△Q or MC(Q)=lim=△TC(Q)/△Q=dTC/dQ(△Q→0) (every bit shown in Figure 1)

In theory marginal costs correspond the increase in total costs (which include both constant and variable costs) as output increases by 1 unit.

Apply in economics [edit]

Economical profit versus accounting turn a profit [edit]

The main objective of accounting profits is to give an account of a company's financial performance, typically reported on in quarters and annually. Equally such, accounting principles focus on tangible and measurable factors associated with operating a concern such as wages and rent, and thus, do not "…infer anything about relative economical profitability."[21] Opportunity costs are not considered in accounting profits as they have no purpose in this regard.

The purpose of calculating economic profits (and thus, opportunity costs) is to assistance in better business conclusion-making through the inclusion of opportunity costs. In this way, a business tin can evaluate whether its decision and the allocation of its resources is cost-effective or not and whether resources should be reallocated.[22]

Simplified instance of comparing economical profit vs bookkeeping profit

Economical profit does not signal whether or non a business decision will brand money. It signifies if it is prudent to undertake a specific determination against the opportunity of undertaking a unlike decision. As shown in the simplified example in the image, choosing to start a business would provide $x,000 in terms of bookkeeping profits. Even so, the decision to beginning a business organisation would provide -$30,000 in terms of economic profits, indicating that the decision to first a business may non be prudent every bit the opportunity costs outweigh the profit from starting a business. In this case, where the acquirement is not plenty to cover the opportunity costs, the chosen option may not be the all-time form of action.[23] When economic profit is aught, all the explicit and implicit costs (opportunity costs) are covered by the total revenue and there is no incentive for reallocation of the resources. This condition is known as normal turn a profit.

Several performance measures of economic profit have been derived to further improve business determination-making such as risk-adjusted return on capital letter (RAROC) and economic value added (EVA), which directly include a quantified opportunity cost to aid businesses in risk management and optimal resource allotment of resources.[24] Opportunity cost, as such, is an economical concept in economic theory which is used to maximise value through better determination-making.

In bookkeeping, collecting, processing, and reporting data on activities and events that occur within an organization is referred to as the accounting bicycle. To encourage decision-makers to efficiently allocate the resources they have (or those who have trusted them), this data is beingness shared with them.[25] As a result, the role of bookkeeping has evolved in tandem with the ascent of economical activity and the increasing complexity of economical structure. Accounting is not only the gathering and calculation of data that impacts a choice, just it also delves securely into the determination-making activities of businesses through the measurement and computation of such data. In bookkeeping, it is mutual practice to refer to the opportunity cost of a determination (option) as a cost.[26] The discounted cash menstruation method has surpassed all others equally the main method of making investment decisions, and opportunity toll has surpassed all others as an essential metric of cash outflow in making investment decisions.[27] For various reasons, the opportunity toll is critical in this form of estimation.

Kickoff and foremost, the discounted charge per unit applied in DCF assay is influenced past an opportunity cost, which impacts project selection and the choice of a discounting rate.[28] Using the firm's original avails in the investment means there is no need for the enterprise to employ funds to purchase the assets, then at that place is no cash outflow. Yet, the cost of the avails must be included in the cash outflow at the current market price. Fifty-fifty though the asset does not result in a cash outflow, it can be sold or leased in the market to generate income and be employed in the project's greenbacks flow. The money earned in the market place represents the opportunity cost of the asset utilized in the business venture. As a upshot, opportunity costs must exist incorporated into projection planning to avoid erroneous project evaluations.[29] Simply those costs directly relevant to the project volition exist considered in making the investment choice, and all other costs will be excluded from consideration. Modernistic bookkeeping besides incorporates the concept of opportunity cost into the determination of capital costs and capital structure of businesses, which must compute the price of capital invested by the owner every bit a function of the ratio of human capital. In addition, opportunity costs are employed to determine to price for asset transfers between industries.

Comparative reward versus absolute advantage [edit]

When a nation, organisation or individual can produce a product or service at a relatively lower opportunity cost compared to its competitors, information technology is said to accept a comparative reward. In other words, a country has comparative advantage if it gives up less of a resource to make the same number of products as the other land that has to give up more.[30]

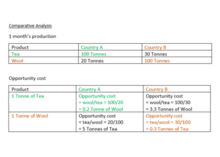

A simple example of comparative advantage.

Using the simple case in the prototype, to brand 100 tonnes of tea, Land A has to give up the production of xx tonnes of wool which ways for every 1 tonne of tea produced, 0.ii tonne of wool has to exist forgone. Meanwhile, to make 30 tonnes of tea, Country B needs to sacrifice the production of 100 tonnes of wool, so for each tonne of tea, 3.three tonnes of wool is forgone. In this case, Country A has a comparative advantage over Country B for the production of tea because it has a lower opportunity price. On the other manus, to make ane tonne of wool, Country A has to give up v tonnes of tea, while State B would need to give up 0.three tonnes of tea, so Country B has a comparative advantage over the product of wool.

Accented advantage on the other manus refers to how efficiently a party tin can employ its resource to produce goods and services compared to others, regardless of its opportunity costs. For instance, if State A can produce one tonne of wool using less manpower compared to Country B, and so it is more efficient and has an accented advantage over wool production, fifty-fifty if it does not have a comparative advantage considering it has a college opportunity cost (5 tonnes of tea).[30]

Absolute reward refers to how efficiently resources are used whereas comparative reward refers to how trivial is sacrificed in terms of opportunity cost. When a land produces what it has the comparative advantage of, fifty-fifty if information technology does not have an accented reward, and trades for those products it does non take a comparative advantage over, it maximises its output since the opportunity cost of its product is lower than its competitors. By focusing on specialising this way, information technology as well maximises its level of consumption.[30]

Opportunity cost at governmental level [edit]

Much like private decisions, it is often the case that governments must consider opportunity cost when enacting legislation. Taking universal basic healthcare as an example, the opportunity cost at the authorities level is quite clear. Assume that implementing basic healthcare would price a government $1 billion: the explicit opportunity cost to implement such legislation would be a combined $ane billion that could take been spent on education, housing, ship infrastructure, ecology protection, or military defence, for example. For this particular scenario, the implicit cost is quite minimal. Only the cost of producing such legislation through homo labour and the time of product would demand to be accounted for.

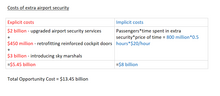

Opportunity cost to implement additional hijacking prevention methods

While the previous situation'south implicit toll may have been somewhat negligible at a government level, this is not true for all scenarios. Using hijacking prevention methods post-obit the September 11 attacks equally an instance, the additional burden of implicit costs is evident. To implement more than sophisticated airport security systems, the The states government estimated the cost to exist around $2 billion. An additional $450 million would be spent to reinforce plane doors, along with an extra $3 billion spent on heaven marshals for all American flights to help farther prevent time to come hijackings from taking place. Under this scenario, the explicit cost would be $5.45 billion. Implicit costs, however, would far outweigh this. The US government has calculated that by waiting an additional 30 minutes due to extra airport security, multiplied by an average of 800 million passengers per year with the average cost of time at $twenty per hour, the total implicit cost to the US economic system from such prevention methods would be upwardly of $viii billion.[31] Thus the importance of recognising the opportunity toll at a governmental level is crucial in efficiently allocating government funds.

Demand and supply of hospital beds and days during Covid-19q

The impact of the Covid-9 pandemic that bankrupt out in contempo years on economical operations is unavoidable, the economic risks are not symmetrical, and the impact of Covid-19 is distributed differently in the global economy. Some industries take benefited from the pandemic, while others accept almost gone broke. I of the sectors most impacted past the COVID-nineteen pandemic is the public and private health system. Opportunity toll is the concept of ensuring efficient utilize of scarce resources,[32] a concept that is key to health economic science. The massive increment in the need for intensive care has largely limited and exacerbated the department'due south ability to address routine health problems. The sector must consider opportunity costs in decisions related to the resource allotment of scarce resources, premised on improving the health of the population.[10]

All the same, the opportunity cost of implementing policies to the sector has limited impact in the health sector. Patients with severe symptoms of COVID-19 require shut monitoring in the ICU and in therapeutic ventilator support, which is primal to treating the affliction.[33] In this case, deficient resources include bed days, ventilation time, and therapeutic equipment. Temporary excess demand for infirmary beds from patients exceeds the number of bed days provided by the health system. The increased need for days in bed is due to the fact that infected hospitalized patients stay in bed longer, shifting the need bend to the right (see bend D2 in Graph1.xi).[32] The number of bed days provided by the health system may be temporarily reduced as in that location may exist a shortage of beds due to the widespread spread of the virus. If this situation becomes unmanageable, supply decreases and the supply curve shifts to the left (curve S2 in Graph1.11).[32]A perfect contest model tin be used to express the concept of opportunity cost in the health sector. [34] In perfect competition, market place equilibrium is understood every bit the point where supply and demand are exactly the same (points P and Q in Graph1.11).[32] The remainder is Pareto optimal equals marginal opportunity cost. Medical allocation may result in some people being better off and others worse off. At this signal, information technology is assumed that the market has produced the maximum outcome associated with the Pareto partial order.[32] Equally a result, the opportunity cost increases when other patients cannot be admitted to the ICU due to a shortage of beds.

See too [edit]

- Austrian School

- Best alternative to a negotiated agreement

- Budget constraint

- Economies of scale

- Econometrics

- Fear of missing out

- Production-possibility frontier

- Reduced cost aka 'opportunity cost' in linear programming

- There ain't no such matter as a gratis lunch

- Time direction

- Trade-off

- Transaction toll

- You lot can't have your cake and consume information technology

- Perverse subsidies

References [edit]

- ^ Fernando, Jason. "Opportunity Price". Investopedia . Retrieved 23 April 2021.

- ^ a b c Buchanan, James Chiliad. (1991). "Opportunity Cost". The World of Economics. The New Palgrave: 520–525. doi:10.1007/978-ane-349-21315-3_69. ISBN978-0-333-55177-6 – via SpringerLink.

- ^ a b "Economics A-Z terms beginning with O". The Economist . Retrieved i November 2020.

- ^ a b Hutchison, Emma (2017). Principles of Microeconomics. Academy of Victoria.

- ^ Pettinger, Tejvan. "Opportunity Cost Definition". Economic science Aid . Retrieved 30 April 2021.

- ^ Perron, Pierre; Bai, Justin (2003). "Computation and analysis of multiple structural change models". Journal of Applied Econometrics. 18: 1–22. doi:10.1002/jae.659. Retrieved 9 May 2022.

- ^ Parkin, Michael (2016). "Opportunity Price: A reexamination". The Journal of Economical Education. 47 (ane): 12–22. doi:x.1080/00220485.2015.1106361. S2CID 155746220 – via Taylor & Francis Online.

- ^ "A HISTORICAL VIEW OVER THE OPPORTUNITY COST -Bookkeeping DIMENSION". ResearchGate . Retrieved 1 November 2020.

- ^ Burch, Earl East.; Henry, William (1974). "Opportunity and Incremental Cost: Attempt to Define in Systems Terms: A Comment. The Accounting Review". The Accounting Review. 49: 118–123. JSTOR 244804 – via JSTOR.

- ^ a b F., Drummond, M. (2005). Methods for the economic evaluation of health care programmes. Oxford University Press. ISBN978-0-nineteen-852945-3. OCLC 300939640.

- ^ a b M., Buchanan, James (1999). Cost and choice : an inquiry in economical theory. Liberty Fund. ISBN0-86597-224-ix. OCLC 476349821.

- ^ a b Robinson, Scharn (twenty April 2017). "Opportunity Costs". University of Illinois Printing. ane. doi:ten.5406/illinois/9780252036453.003.0008.

- ^ a b c "Explicit and implicit costs and accounting and economic profit". Khan University. 2016. Retrieved 1 Nov 2020.

- ^ a b "Explicit Costs - Overview, Types of Profit, Examples". Corporate Finance Constitute . Retrieved thirty April 2021.

- ^ a b c d "Explicit Costs: Definition and Examples". Indeed. 5 February 2020. Retrieved 1 November 2020.

- ^ a b Crompton, John L.; Howard, Dennis R. (2013). "Costs: The Residuum of the Economical Impact Story" (PDF). Journal of Sport Management. 27 (v): 379–392. doi:x.1123/JSM.27.v.379. S2CID 13821685. Archived from the original (PDF) on 4 March 2019.

- ^ a b Kenton, Will. "How Implicit Costs Work". Investopedia . Retrieved 30 April 2021.

- ^ a b "Reading: Explicit and Implicit Costs". Lumen Learning . Retrieved one November 2020.

- ^ Devine, Kevin; O Clock, Priscilla (March 1995). "The effect on sunk costs and opportunity costs on a subjective uppercase allocation decision". The Mid-Atlantic Periodical of Business. 31 (one): 25–38.

- ^ "4 Examples of Sunk Cost". Indeed. 6 October 2020. Retrieved 1 November 2020.

- ^ Holian, Matthew; Reza, Ali (nineteen July 2010). "Firm and industry effects in bookkeeping versus economic profit data". Practical Economics Messages. eighteen (6): 527–529. doi:x.1080/13504851003761756. S2CID 154558882.

- ^ Goolsbee, Austan; Levitt, Steven; Syverson, Chad (2019). Microeconomics (3rd ed.). Macmillan Learning. pp. 8a–8j. ISBN9781319306793.

- ^ Layton, Allan; Robinson, Tim; B. Tucker Iii, Irvin (2015). Economics for Today (5th ed.). Cengage Australia. pp. 131–132, 479–486. ISBN9780170276313.

- ^ Kimball, Ralph (1998). "Economic Profit and Functioning Measurement in Banking". New England Economical Review. Federal Reserve Bank of Boston: 35–39. ISSN 0028-4726. Retrieved 13 March 2021.

- ^ P., Magee, Robert (1986). Avant-garde managerial accounting. Harper & Row. OCLC 1287886441.

- ^ C., Vera-Munoz, Sandra (1998). The effects of accounting knowledge and context on the omission of opportunity costs in resources allocation decisions. American Bookkeeping Association. OCLC 926973835.

- ^ "Accounting and the theory of the business firm*", The Firm as an Entity, Routledge, pp. 94–103, 12 Apr 2007, doi:10.4324/9780203931110-thirteen, ISBN9780429240607 , retrieved 2 May 2022

- ^ Chung, Kee H. (1 May 1989). "Inventory Control and Trade Credit Revisited". Periodical of the Operational Research Society. 40 (v): 495–498. doi:10.1057/jors.1989.77. ISSN 0160-5682. S2CID 16422604.

- ^ South.), Herroelen, Willy (Willy (1995). Projection network models with discounted greenbacks flows : a guided tour through recent developments. Katholieke Universiteit Leuven, Departement Toegepaste Economische Wetenschappen. OCLC 68978777.

- ^ a b c Layton, Allan; Robinson, Tim; B. Tucker 3; Irvin (2015). Economics for Today (5th ed.). Cengage Australia. pp. 131–132, 479–486. ISBN9780170276313.

- ^ Jones, Peter. "The Concept of Opportunity Cost". ER services . Retrieved 25 April 2021.

- ^ a b c d e Olivera, Mario J. (29 December 2020). "Opportunity cost and COVID-nineteen: A perspective from health economics". Medical Journal of the Islamic Commonwealth of Iran. 34: 177. doi:10.47176/mjiri.34.177. ISSN 1016-1430. PMC8004566. PMID 33816376.

- ^ World Health Organisation (20 May 2020). "Clinical management of astringent acute respiratory infection (SARI) when COVID-19 illness is suspected. Acting guidance". Pediatria I Medycyna Rodzinna. 16 (1): 9–26. doi:x.15557/pimr.2020.0003. ISSN 1734-1531. S2CID 219964509.

- ^ A., Lipsey, R. G. Chrystal, Chiliad. (2007). Economics. Oxford University Press. ISBN978-0-19-928641-half dozen. OCLC 475315028.

External links [edit]

- The Opportunity Cost of Economics Education by Robert H. Frank

What Cost Is Not Included In The Real Prices Of Goods And Services?,

Source: https://en.wikipedia.org/wiki/Opportunity_cost

Posted by: walshthowelf1956.blogspot.com

0 Response to "What Cost Is Not Included In The Real Prices Of Goods And Services?"

Post a Comment